Ever feel like your bank account has a mind of its own? Turns out, you're not alone. New research out of Australia suggests that when it comes to money, young adults aren't just good or bad with it — they fall into distinct "money behavior types." And simply knowing a few financial facts isn't going to change them.

Researchers from Southern Cross University, QUT, and Griffith University wrangled 519 Australians aged 18–35. Their mission: to map the actual financial habits of people fresh into their careers, a time when money habits tend to crystallize for life. The result? Three distinct tribes, each with their own quirks and financial outcomes.

The study, published in the Pacific-Basin Finance Journal, looked at everything from saving and investing to budgeting and the wonderfully modern world of buy-now-pay-later apps. Because apparently, that's where we are now.

We're a new kind of news feed.

Regular news is designed to drain you. We're a non-profit built to restore you. Every story we publish is scored for impact, progress, and hope.

Start Your News DetoxMeet Your Money Type

So, which tribe claims you? Let's break down the cast of characters:

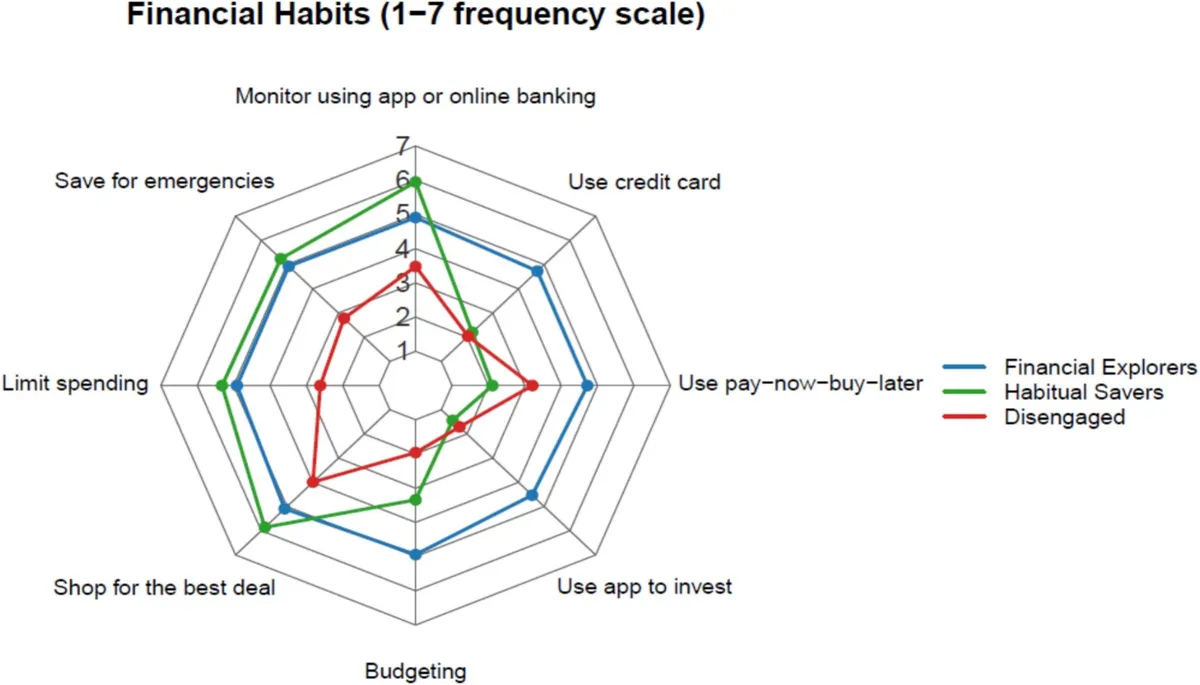

Financial Explorers: These folks are the hyper-engaged, often overly confident ones. They're budgeting, saving, investing, and probably have three different financial apps open right now. They're also the most likely to use buy-now-pay-later schemes, which, if you think about it, is both impressive and slightly terrifying.

Habitual Savers: The cautious optimists. They're all about traditional saving, avoiding debt like it's a plague, and generally feeling pretty good about their spending control. The downside? They might be missing out on opportunities to grow their wealth long-term because they're a bit gun-shy about investing.

The Disengaged: Ah, the classic "head in the sand" approach. This group does minimal financial planning, budgeting, or regular saving. Yet, ironically, they're still likely to rack up debt or dive into buy-now-pay-later. Unsurprisingly, they report the highest levels of financial stress. Because, well, math.

Dr. Jennifer Harrison, the lead author, points out that this isn't about ranking who's 'best' with money. It's about recognizing that a one-size-fits-all approach to financial education is about as effective as a chocolate teapot. People have different habits, confidence levels, and social influences shaping their money moves.

Essentially, your upbringing and personality probably already set the stage for your financial dance moves. Starting a full-time job doesn't magically reset everything.

So, what's the takeaway? Instead of generic advice, we need tailored solutions. Financial Explorers might need a reality check on risk assessment. Habitual Savers could use a gentle nudge toward smart investing. And The Disengaged? They probably need simple tools to reduce stress and build those foundational habits. Because who doesn't want to feel a little less stressed about their bank balance?